What we do

Investment

Outperform the market by appointing our exceptionally well-connected investment experts.

Outperform the market by appointing our exceptionally well-connected investment experts to acquire or dispose of your property assets with transactions completed at the right market level for you

We can support you on a national investment strategy, and on a location or industry specific individual transaction by driving the best possible outcome. Our market facing experts will partner with you to negotiate the best deals for your business. Similarly, our connections to both buyers and vendors give clients unique access to off-market opportunities providing you with competitor advantage.

With the support of our industry specialist agency and consultancy teams we are able to add value to your strategy. We pride ourselves on thinking creatively and proposing new opportunities that others won’t have considered.

Get in touch

Key contacts

Gain national and local expertise through our multidisciplinary teams of experts.

Featured properties

Automotive & Roadside

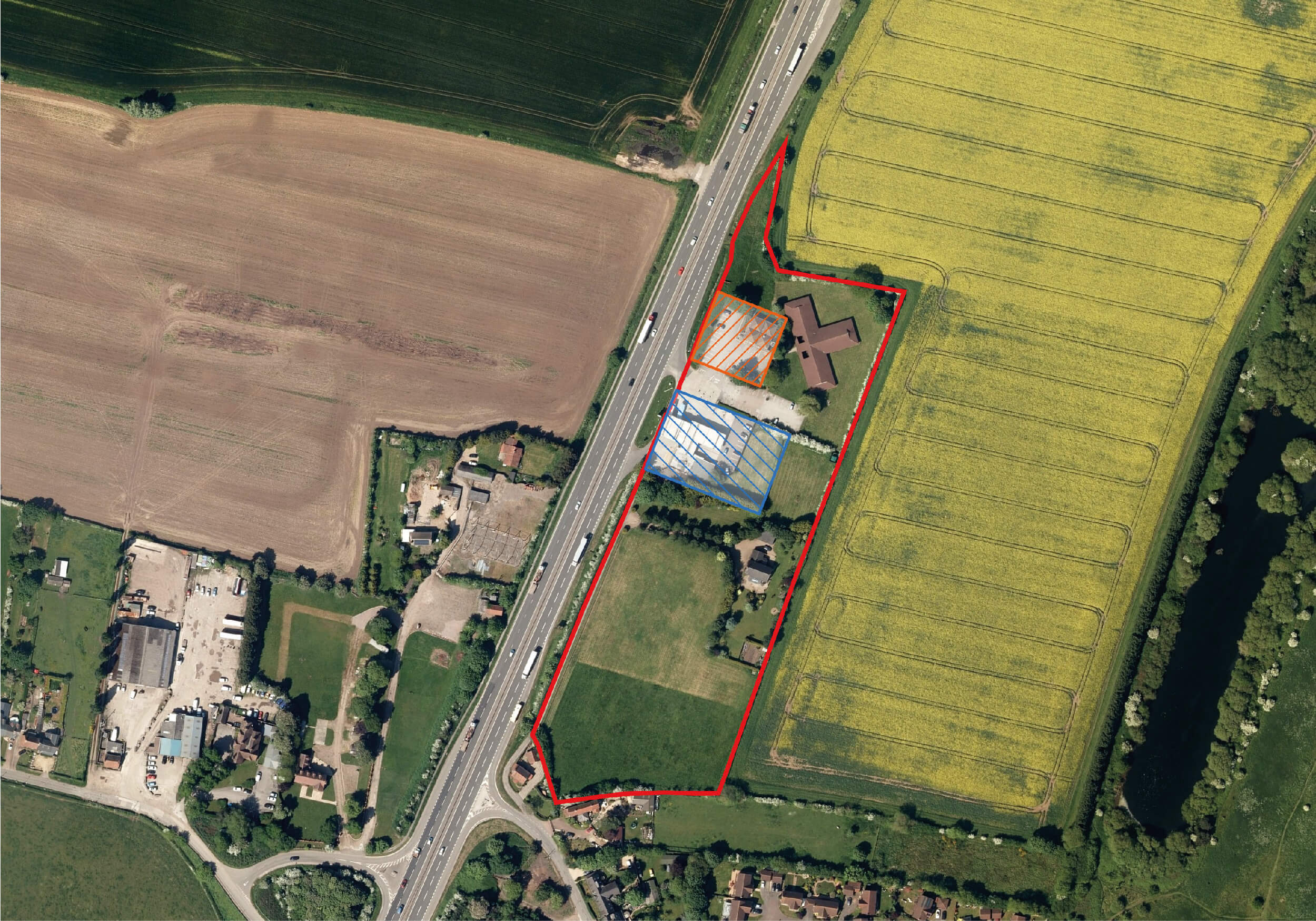

Roadside Service Area Investment with Development Potential – Newark

Muskham Services, A1 Southbound, Newark, NG23 6HT

For Sale

32,293 sq m (347,598.96 sq ft)

Prime Dealership Investment with RPI Linked Rent Reviews

Volvo, Chester Road, Erdington, B24 0QY

Our track record

URC Thames North Trust

Freehold interest sale of United Reform Church Thames North, Camden, London

Private Client

International retailer’s non-operational property portfolio

Proactively managed the portfolio to maximise value and minimise risk

CBRE Global Investors

Investment acquisition, Basingstoke

Identified a semi off market foodstore opportunity for a longstanding client

Lookers Plc

Investment sale, Battersea

Sale and leaseback for a state of the art flagship Volkswagen car dealership

Private Client

Proactive cost mitigation for a national retailer

Delivered cost mitigation for a portfolio of circa 500 UK retail outlets

Lookers Plc

Redevelopment of York Road, Battersea

Instructed to maximise the redevelopment potential of a VW site

Related News

Rapleys names Rebecca Harper Head of Investment

UK, January 2024 – Rapleys has named Rebecca Harper as Head of Investment within the Partnership’s Commercial Division.